Macro Monthly: Data Reality vs. Headline Fiction

Hi people, it’s René Steiner from SteinerCapital. Below you will find my latest research and views on markets. Note that this is NEVER financial advise.

Key Takeaways

While the expectations are clearly towards a stagflation backdrop for western and asian economies alike, the data does not confirm this expectation just now

AUD, JPY reflation; USD, GBP, EUR, NZD Goldilocks; CHF, CAD Deflation

These conclusions are the current base case but are subject to change as soon as the data changes

Introduction

This publication provides a structured, cross-jurisdictional assessment of the global macro landscape. Our focus remains on the core G10 economies most relevant for institutional asset allocation and FX overlay strategies: the US, Eurozone (proxying via Germany where necessary), Japan, UK, Switzerland, Canada, Australia, and New Zealand.

We utilize a standardized analytical framework, prioritizing leading indicators for inflation and real economic activity. These signals are benchmarked against central bank reaction functions and forward guidance to synthesize a coherent trajectory for global monetary policy.

The Objective:

Momentum Mapping: Identifying underlying macro shifts across regions before they are fully priced in.

Trade Translation: Distilling macro data into actionable FX views evaluating both directional bias and relative value (RV) opportunities.

Looking at Inflation

The drivers of the current inflationary impulse are multifaceted and frequently contested. Rather than chasing a single "root cause," our objective is pragmatic: we assess the evolution of key macro variables and their implications for the inflationary process across developed markets (DM). We decompose these dynamics into global vs. local components, further isolating volatile headline drivers from core stickiness.

Global Components

In the current cycle, inflation remains (first and foremost) a global phenomenon. While idiosyncratic domestic outcomes persist, the dominant price impulses are driven by synchronized global forces, amplified or dampened by local fiscal policy and structural labor market rigidities.

Volatile Inflation Components

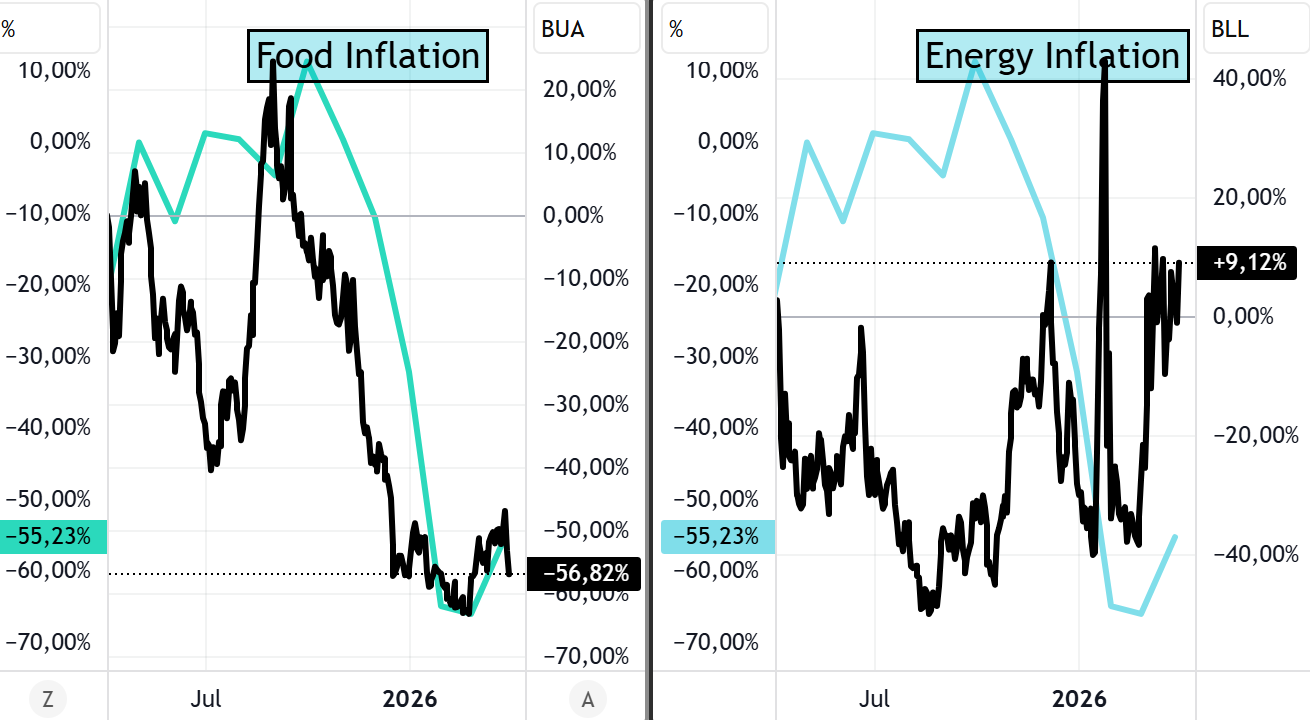

Our proprietary proxies for global food and energy inflation currently present a bifurcated backdrop. While the food disinflation narrative remains intact (for now), the escalation of the US-Iran conflict has introduced a violent bid into energy markets. The disinflationary tailwinds identified in our February report have effectively evaporated.

If this energy price shock remains “sticky” at spot levels (or accelerates further) we risk a rapid reversal of the disinflationary progress seen over the last two quarters.

On a Year-Over-Year basis our proprietary food indicator remains at -50%, which continues the disinflationary story but the energy proxy tells a different one. On a YoY Basis the proxy is up 10%, which is a rapid increase from February.

Global Core Components

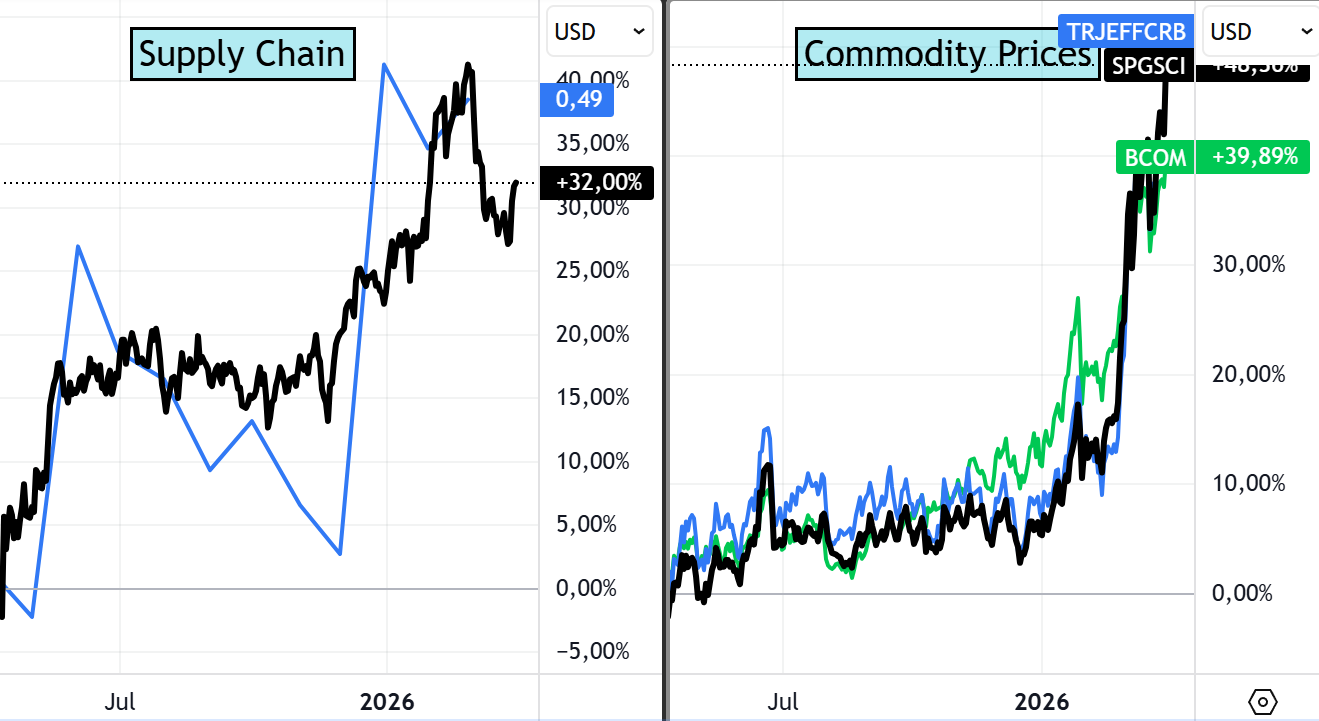

The inflationary impulse stemming from the US-Iran conflict is gaining additional convexity when viewed through the lens of supply chain pressure and broad-based commodity indices. We are currently observing a synchronized acceleration in both.

Now the supply chain pressure index from NYFED shows a 32% increase YoY and depending on the commodity basket the increase ranges from 30% to 150%.

Thats insane.

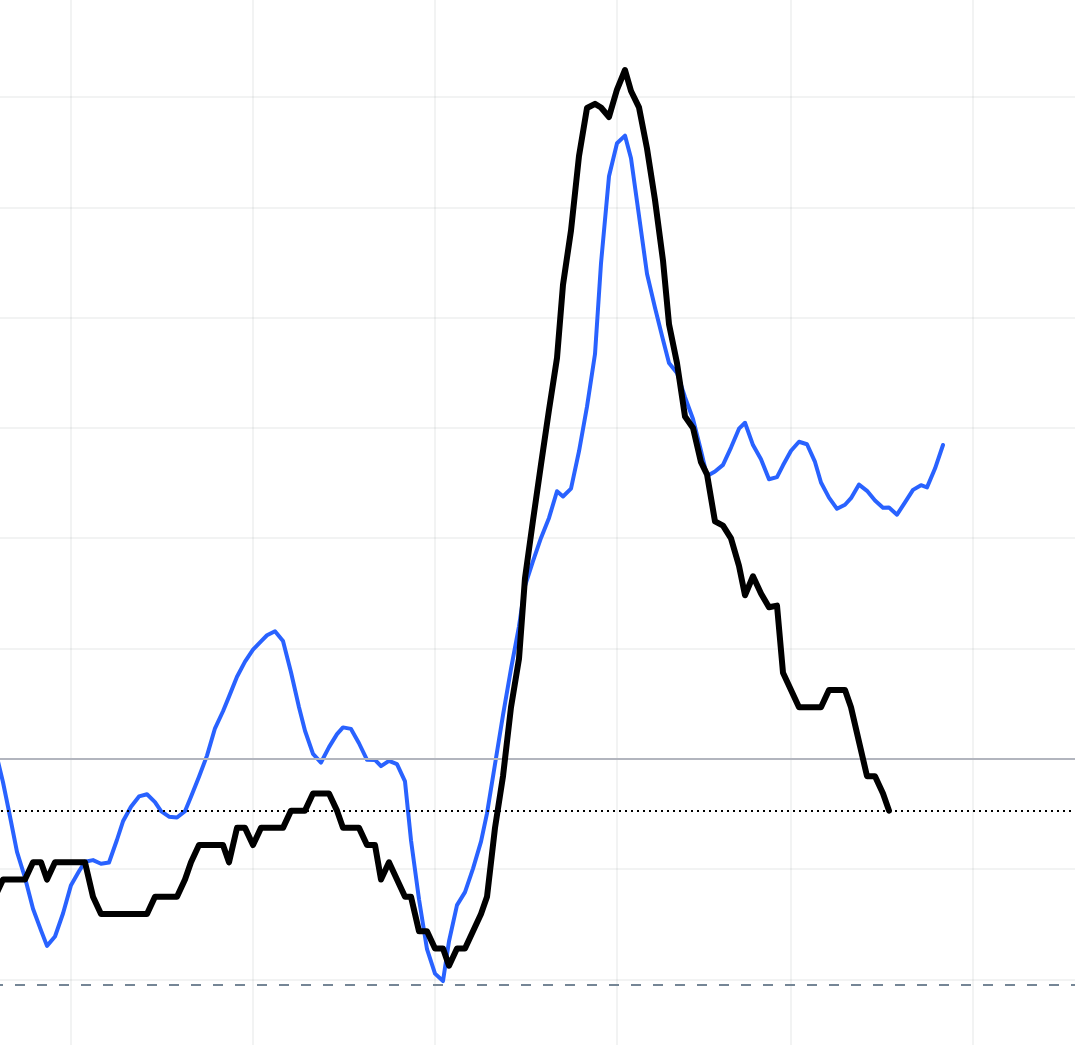

As you can see in the chart below, there is a clear correlation with a small lead time of about 6 months from commodities (SPGSCI - Blue Line) to Headline Inflation for the US(Black Line).

True, it is not always the case and especially on the downside inflation doesnt always feed trough, but it is only logical that increases will be pushed trough the consumers at the end.

I am working on a dedicated article towards forecasting inflation with the tools at hand, if this sounds interesting to you sub to the channel to not miss it:

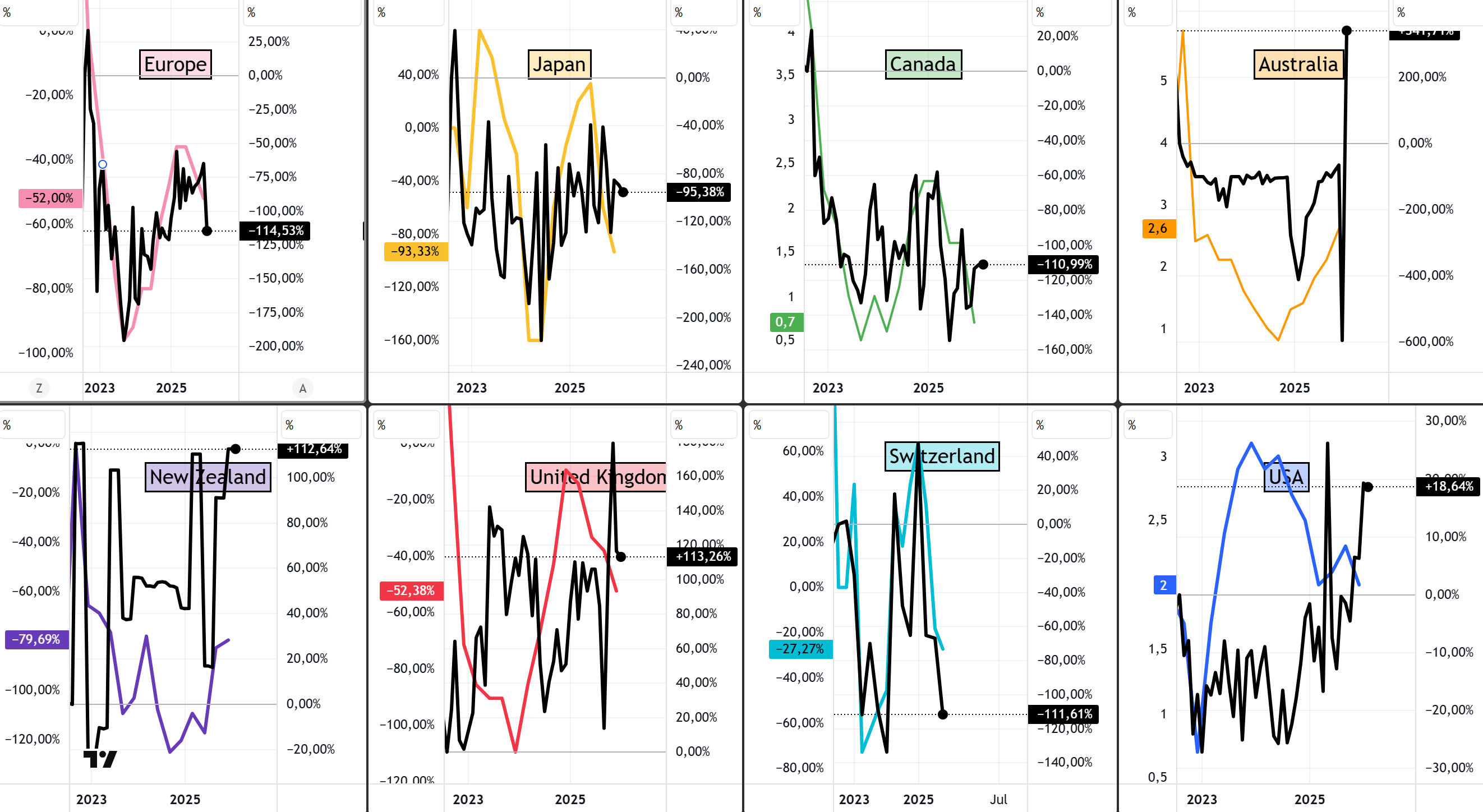

Ideosyncratic Inflation Components

While global tailwinds establish the baseline, domestic variables remain the definitive swing factors for central bank reaction functions. Our proprietary proxies for Wage Growth (Black Line) and House Price Measurments (Blue Line) (both measured on a year-over-year basis) continue to signal a structural disinflationary trajectory across the core of Developed Markets (DM).

At the sovereign level, the data reveals a stark divergence in momentum. In the United States, United Kingdom, and Canada, the synchronized cooling of both labor costs and housing valuations reinforces the disinflationary narrative. Conversely, the "Rest of World" coverage tells a different story. Switzerland, Australia, and Japan are witnessing an acceleration in wage growth. Simultaneously, house prices are gaining renewed traction across the Eurozone, New Zealand, Australia, and Japan.

Key Takeaways

The current landscape is defined by fragmented inflationary impulses rather than a monolithic global trend.

Energy as renewed Catalyst: Upward pressure on energy benchmarks is increasingly evident. These input costs are poised to permeate the broader economy, driving price hikes from logistics to consumer staples, which risks triggering secondary effects—most notably, renewed wage demands.

The Asian Outlier: Inflationary forces are intensifying in key Pacific economies, specifically Japan and Australia. In these jurisdictions, both idiosyncratic proxies (wages and housing) are trending upward, defying the broader cooling seen elsewhere.

Western Resilience vs. Deceleration: This stands in direct contrast to the US, UK, and Canada, where a gradual disinflationary process remains the case (at least until the hard data mandates a pivot in thesis).

The Divergence Gap: A notable tension exists in the Eurozone, Switzerland, and New Zealand. In these regions, the proxies are flashing conflicting signals, with one metric pointing toward reflation while the other suggests continued cooling, complicating the path forward for local policymakers.

Looking at GDP

How GDP works for the coverage

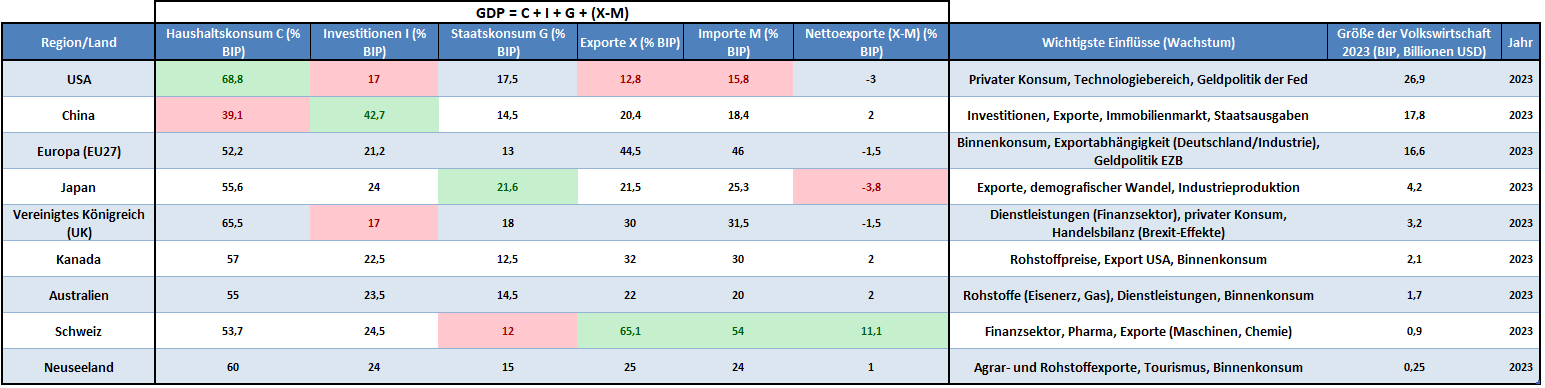

In macro analysis, growth is never monolithic. We recognize that domestic consumption, global trade exposure, and fiscal multipliers vary significantly across our coverage. To isolate these idiosyncratic risks, we decompose GDP into its core engines: Consumption, Investment, Government Spending, and Net Exports.

The Structural Map:

United States: The quintessential consumption-driven powerhouse. Its low relative exposure to global trade explains why the US remains the “cleanest shirt in the dirty laundry” during global tariff wars.

China: Investment remains the primary alpha driver, leaving the tape highly sensitive to Beijing’s credit impulses and infrastructure cycles.

Japan: Fiscal policy is the dominant variable. Government support plays a outsized role, making the macro outlook a function of Diet elections and geopolitical positioning.

United Kingdom: A bifurcated story of a resilient consumer sector battling structurally lethargic investment dynamics.

The “Commodity Trio” (AUD, CAD, NZD): Shared DNA. These economies are effectively a levered play on commodity cycles, housing, and external demand.

Eurozone & Switzerland: High beta to global trade. Their export-heavy models explain why they are the primary victims of any “America First” protectionist tilt.

Cyclical GDP

To front-run the "lagging" nature of official GDP prints, we utilize a Cyclical Proxy (Black Line) composed of New Orders, Industrial Production, and Housing Activity.

The current data reveals a highly fragmented global backdrop. While Canada, Europe, and Switzerland appear to be entering a deflationary phase in activity, Japan remains mired in stagnation. In contrast, the remainder of our coverage—Australia, New Zealand, the UK, and the US—is exhibiting resilient growth profiles, defying broader cooling expectations.

Purchasing Manager Indices

PMIs remain the gold standard for macro investors. The latest S&P Global Manufacturing data confirms several key themes:

USD: Growth momentum is firmly intact; cyclical deterioration has yet to materialize in the hard data.

EUR: Structural headwinds persist, with the bloc struggling to generate any meaningful or sustained expansion.

JPY: Green shoots are emerging, suggesting a potential inflection point, though we await further prints for confirmation.

GBP: Clear evidence of a renewed cyclical upswing.

CHF: Stagnation remains the baseline. While the most recent print showed an aggressive spike, the burden of proof remains on the “sustainability” of that move.

CAD: Persistent weakness continues to validate the bearish signals from our cyclical GDP proxies.

AUD: Robust momentum; forward-looking indicators continue to trend higher.

NZD: Three consecutive strong prints underpin a decidedly constructive growth outlook.

Commentary

I know that under the current lense of rapid Energy price increase, it seems odd to come to such conclusions. But the data shows what the data shows. Until it shows something else, I cant help but conclude this way.

This is the key difference between assumptions and reality. This is why central banks dont hike immediatly when something happens. They have to wait until the data reflects certain dynamics and changes. Everything else would be guess work (which it is anyway) and you dont do guess work on an entire economy.

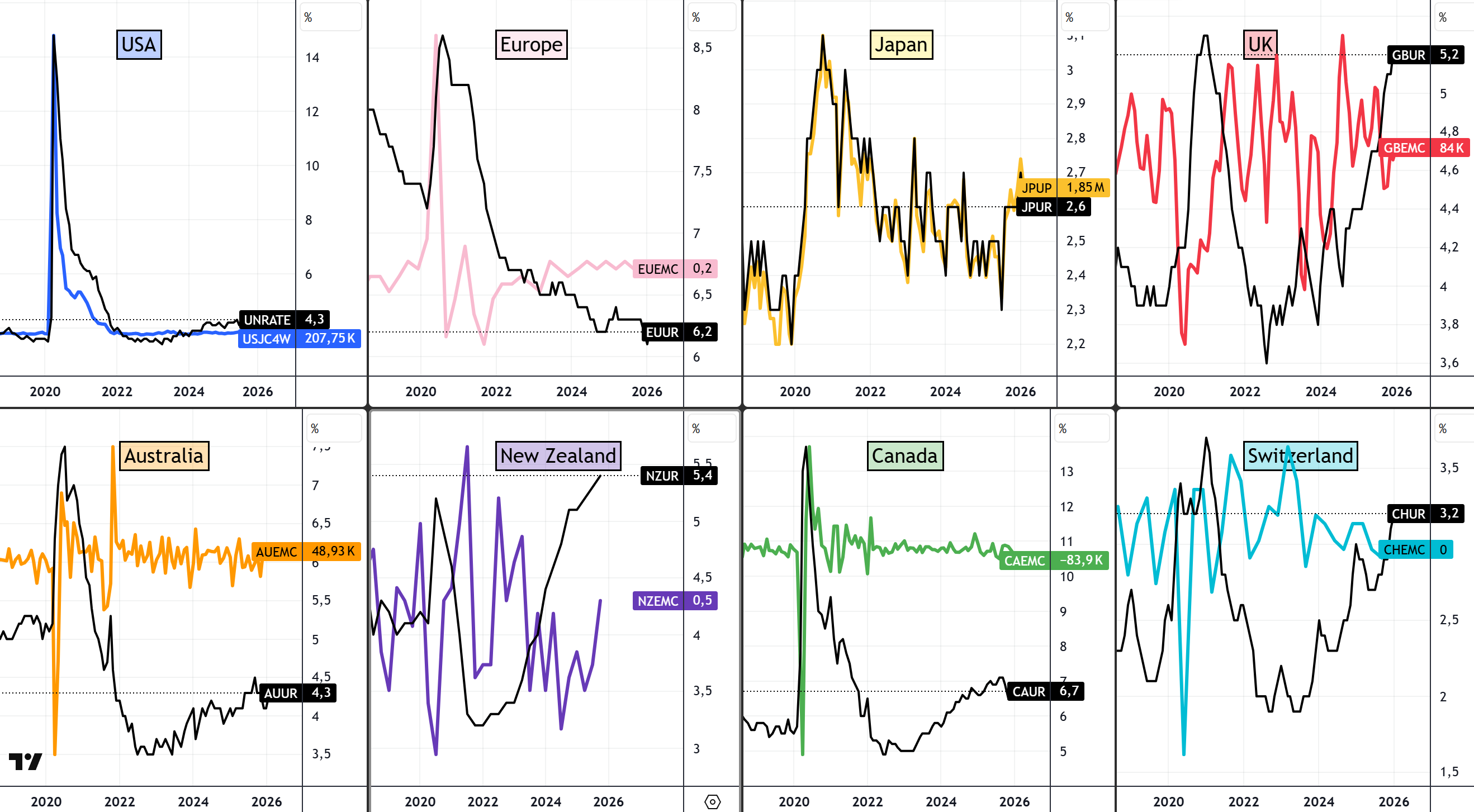

Looking at the Labor Market

Labour market indicators are, at best, coincident and often lagging. As such, they are not a primary driver in this framework. That said, they remain highly relevant from a policy perspective, given the weight central banks place on employment conditions when calibrating monetary settings.

The chart below compares the unemployment rate (black line) with jobless claims or equivalent labour market stress indicators (coloured lines) across the coverage universe

From a historical perspective, the current state of the labor market presents a fascinating paradox: the unemployment rates in New Zealand and the United Kingdom have effectively retraced to pandemic-era levels. This shift signals that the post-Covid “buffer” has largely evaporated in these jurisdictions.

Since the post-pandemic trough of 2023, we have observed a synchronized, albeit gradual, softening of labor markets across the United States, United Kingdom, Canada, Australia, and New Zealand.

Europe, however, remains a glaring outlier. Unemployment across the Eurozone continues to hover at record lows, maintaining a resilience that stands in stark contrast to the continent’s anemic growth profile. In my view, this stability is increasingly atypical and bears the hallmarks of a “borrowed time” scenario. The disconnect between stagnant industrial output and a tight labor market is a structural tension that cannot persist indefinitely.

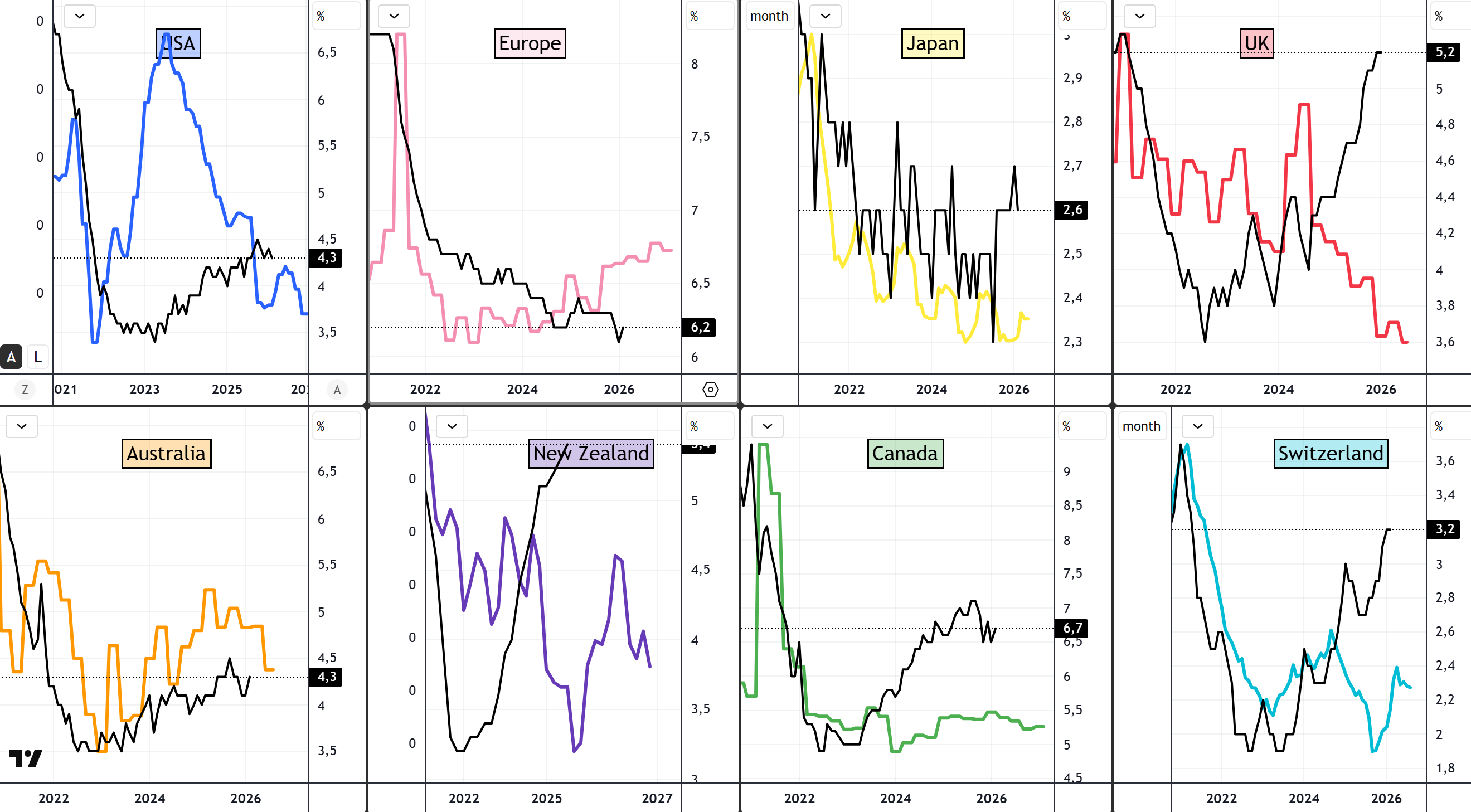

Forecasting the Unemployment Rate

To forecast the unemployment rate, we look at the Ratio of Labor Costs to Corporate Profits. This metric is a powerful lead for corporate behavior; when margins compress, labor—the largest adjustable cost—is usually the first to be "optimized.”

Europe: Our model suggests a significant risk of an upward inflection in unemployment in the coming quarters as the lag between profit compression and layoffs expires.

The Rest of the World: Conversely, in other major economies, unemployment appears more likely to stabilize or ease, buoyed by improving cyclical momentum and a recovery in margins.

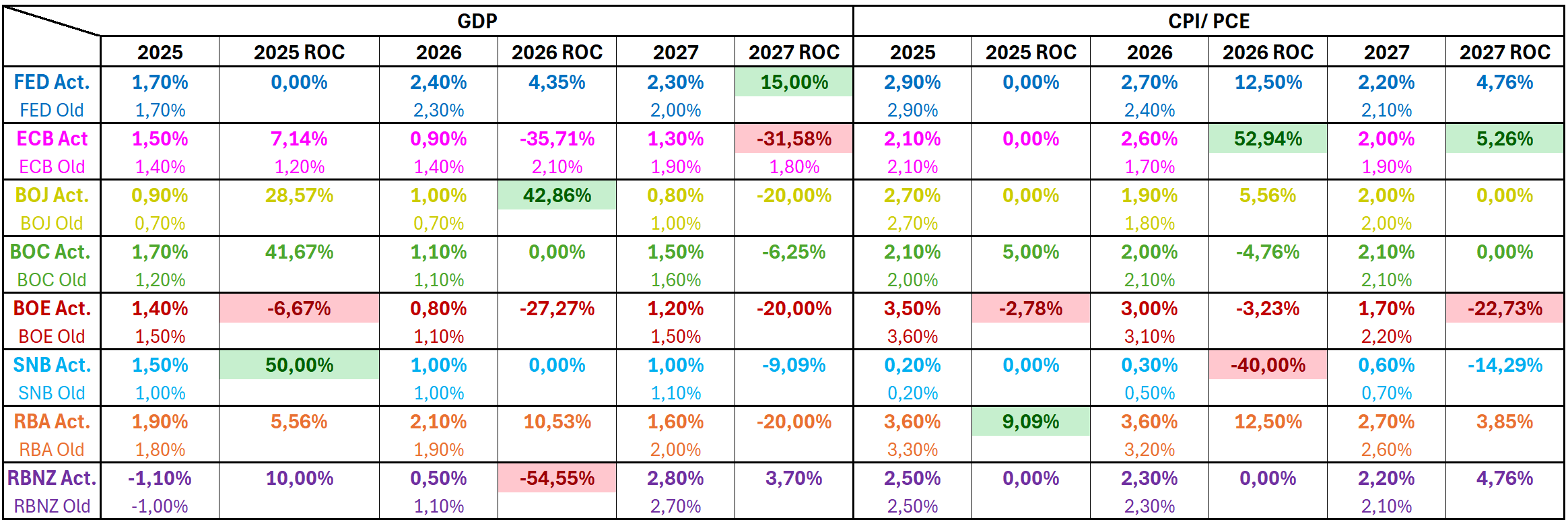

Mapping Central Banks Policy

As outlined in the framework, central banks remain the most informed macro forecasters for their respective economies. They combine privileged data access with country-specific econometric models that are far more granular than any top-down alternative. Ignoring their projections when forming a policy view is therefore suboptimal. While central bank forecasts are not infallible, they provide a critical anchor for interpreting incoming data and market reactions.

Central Bank Projections

Fed: Growth with a glide path to target inflation.

ECB/RBA: Projected increase in Inflation - this is where hawkish risk lays

BOJ/RBNZ: Projecting a reflationary rebound in 2026-27

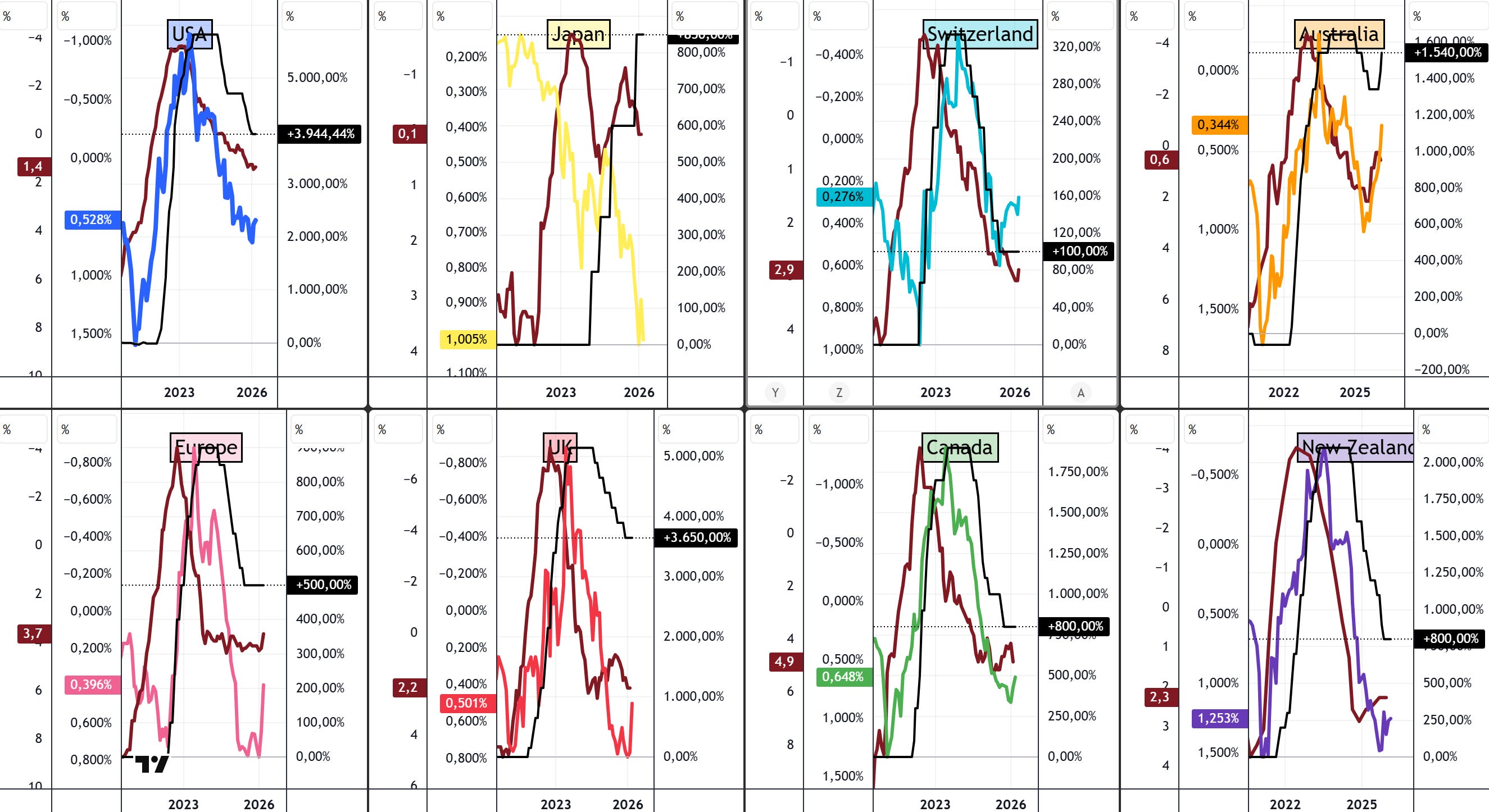

Lagging Indicators lead the key interest rate

To anticipate where central banks might steer rates, we look at the following:

The Model Signal (Brown): The inverse relationship between the unemployment rate and inflation.

The Market Signal (Colored): The 2s10s yield curve spread.

The Yield-Curve Signal

In the wake of the recent surge in energy benchmarks, the subsequent flattening of the yield curve is a textbook mechanical response. This price action serves as a precursor to a further tightening of financial conditions and, by extension, a more restrictive central bank posture.

It is important to note the temporal mismatch here: while yields are re-rated in real-time, official inflation prints are lagging indicators, reflecting the dynamics of the prior month. Consequently, the yield curve is currently front-running the signal while our internal models await the hard data refresh. This does not invalidate our framework; it simply highlights the standard lead-lag relationship between market pricing and realized economic prints.

Policy Signals from the Model

The current output suggests a starkly bifurcated policy path, categorized by the following risk profiles:

Upside Risk (The Reflation Thesis): Australia and New Zealand are the primary outliers. In both jurisdictions, the signals converge on a potential requirement for additional tightening or, at the very least, a definitive “Higher-for-Longer” trajectory. The UK and Canada are exhibiting tentative upside momentum, though we lack the conviction to call for a regime shift just yet.

Downside Risk (The Easing Bias): In the United States, Switzerland, and Japan, the pre-energy shock disinflationary trend remains the dominant force. The underlying data in these regions continues to support the case for a measured easing cycle, provided energy volatility does not become structural.

Policy Inertia (The Holdouts): Europe, Canada, and the UK appear trapped in a low-velocity regime characterized by stagnant growth and contained price pressures. This suggests that “on hold” remains the path of least resistance for local policymakers. While this assessment is subject to revision as energy costs permeate the data, we trade the model as it stands today.

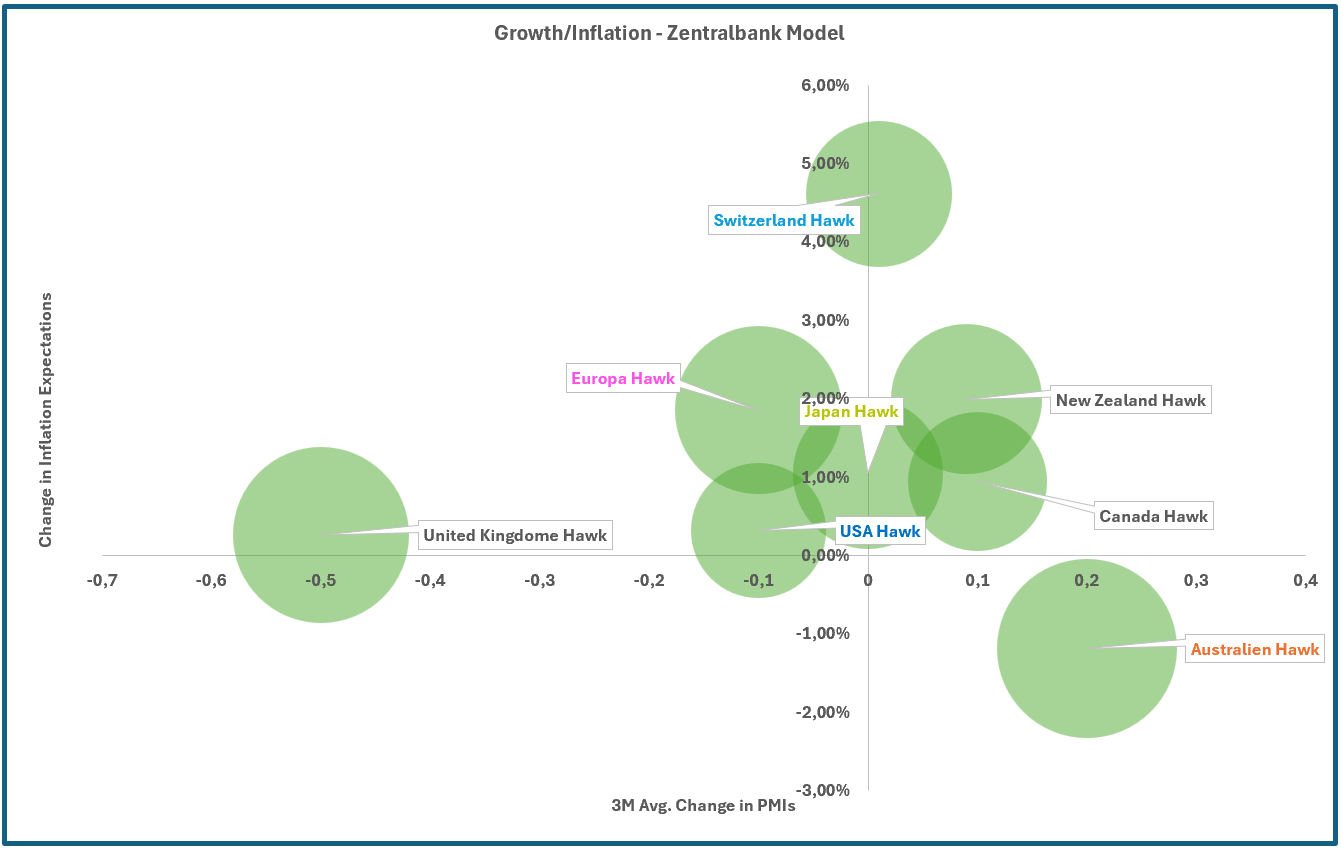

Combining Growth, Inflation and Central Banks

A necessary disclaimer: PMI and Inflation Expectation data are survey-based and were captured pre-US-Iran escalation. In a world of "Triple-Digit Oil" risk, their current validity is under heavy scrutiny. However, the delta in these figures still provides a baseline of where the momentum was heading before the geopolitical shock.

Condensing the data above into one chart, you would get something like this. Here we have a very dense visualization of the growth/inflation dynamics and central bank policy.

Bare in mind, this chart uses the rate of change of these measurments, not the prints itself.

Global Liquidity

This section explores systemic liquidity conditions and transmission channels. While still experimental, it provides useful context for understanding asset price behaviour and policy effectiveness.

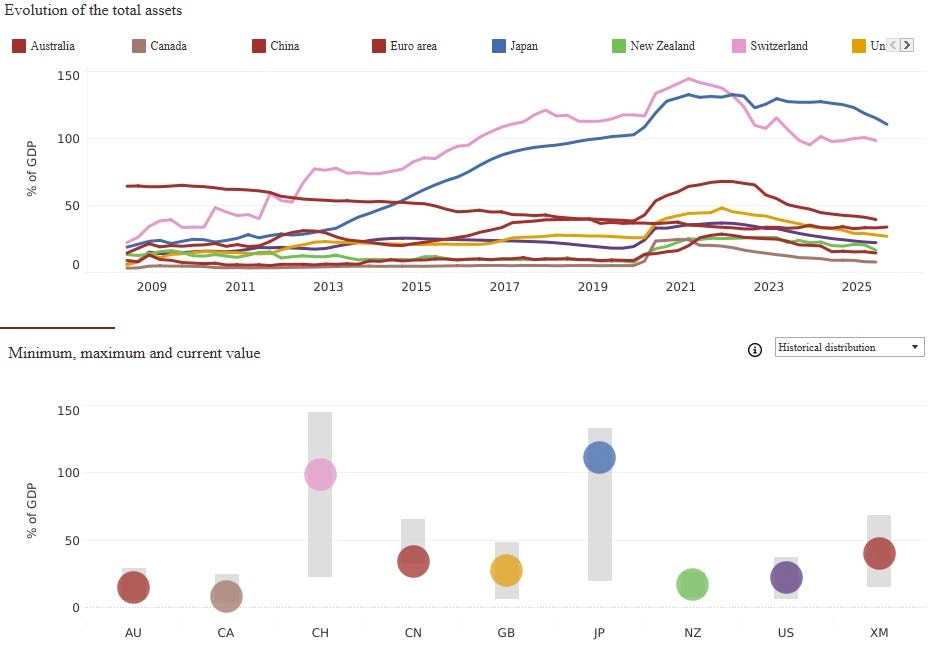

Systemic Liquidity

Since 2021, we’ve lived in a QT regime. While the “normalization” narrative is popular, the reality is that the active tightening impulse has faded. We aren’t in a liquidity crunch yet, but the “Easy Money” tide has clearly receded.

Net Liquidity

Deployable cash is declining. The S&P 500 rally since "Liberation Day" has occurred against a backdrop of lower net liquidity. This implies the rally is driven by earnings multiples and valuation re-ratings—not a central bank liquidity injection. This makes the market vulnerable to any sudden "Risk-Off" deleveraging.

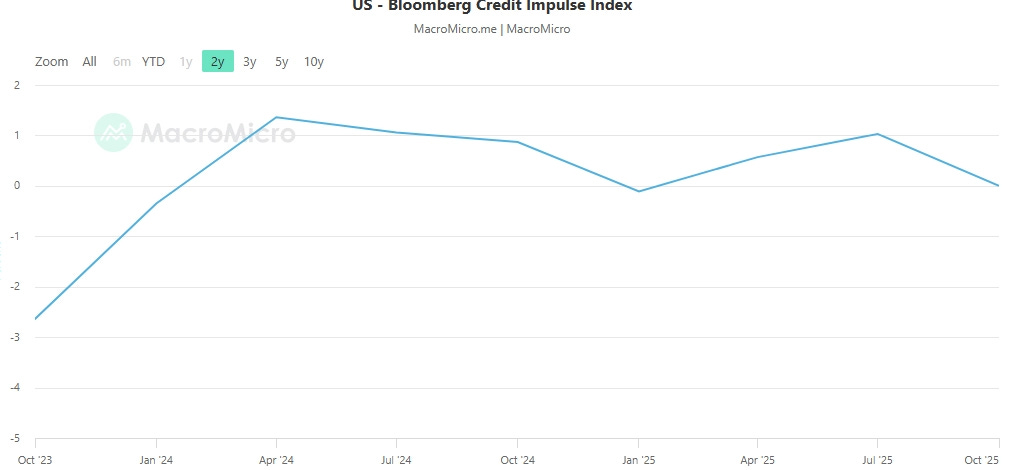

Credit Creation and Transmission

Despite substantial rate cuts by the Fed, private-sector credit creation remains subdued. The credit impulse suggests that borrowing activity has not materially expanded, implying one or more of the following:

The real economy has limited immediate demand for credit

Borrowers perceive rates as still restrictive and are waiting for further easing

Monetary transmission remains impaired, with lower policy rates not fully reaching the real economy

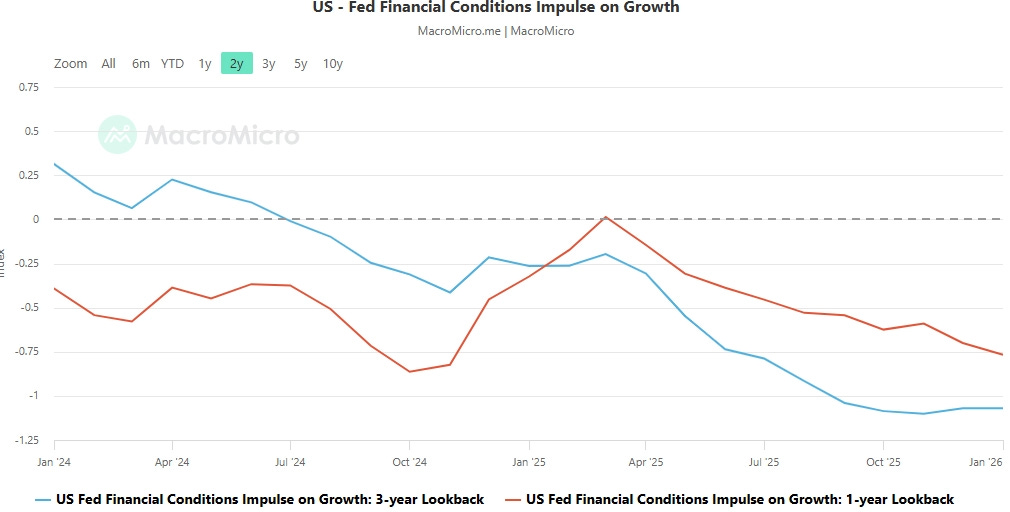

Financial Conditions Indices linked to growth have remained in restrictive territory since Liberation Day. This is notable given multiple policy rate cuts over the same period. The implication is that an easier policy has not translated into easier financial conditions, reinforcing the view that transmission mechanisms remain weak.

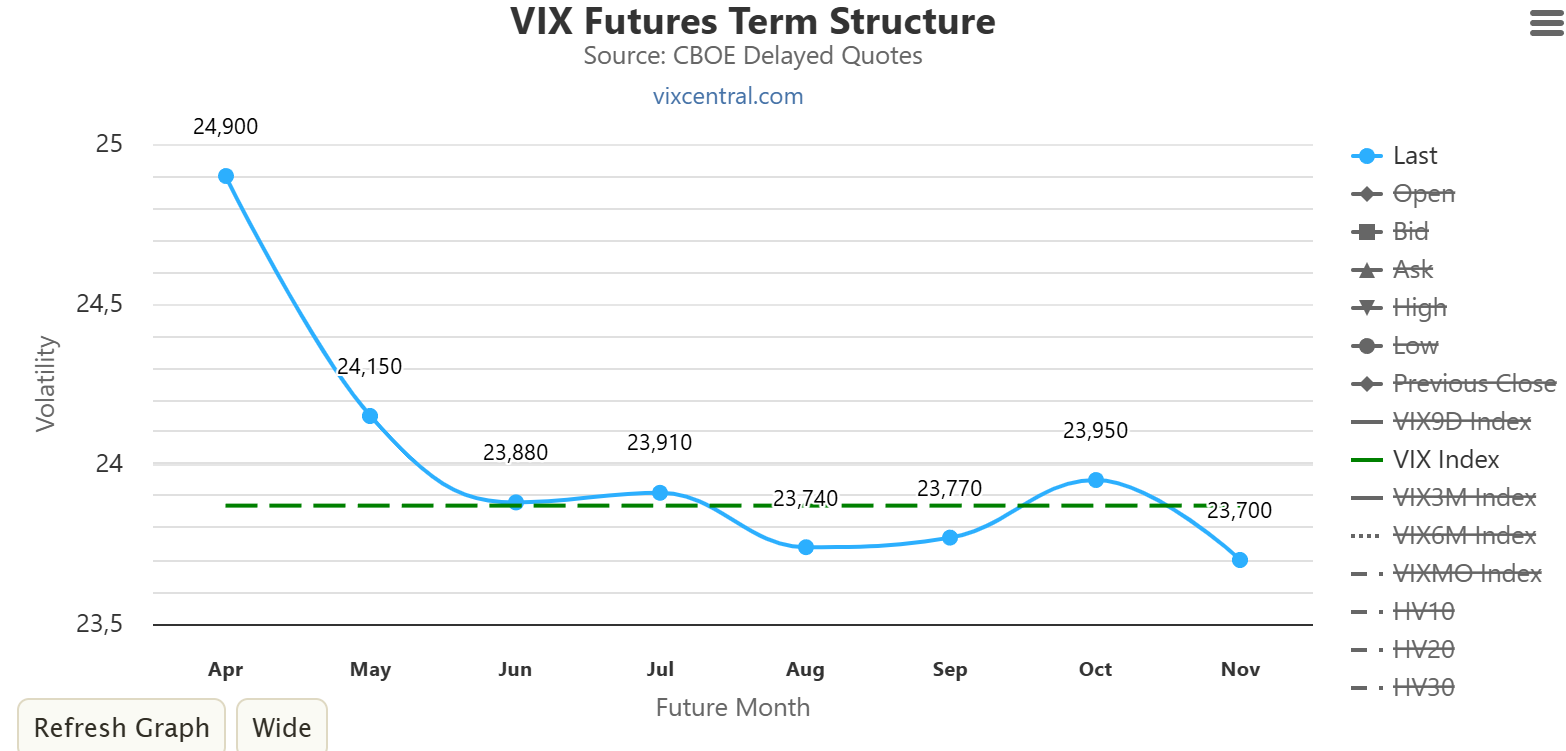

Volatility Analysis

The VIX Term Structure is still in significant backwardation. This is a classic "Front-End Panic" signal, directly tied to the US-Iran escalation.

Key Takeaways

The core takeaway is not that the system is "tight," but that policy easing is failing to propagate. Central banks were cutting, but the real economy isn't feeling the relief. This disconnect explains why growth remains resilient in pockets but fragile at the core.

Final Output

To translate this mountain of data into a coherent narrative, we map the G8 economies across two primary dimensions - Growth and Inflation - and then overlay Central Bank (CB) Reaction Functions. This allows us to identify regime shifts and cross-country relative value (RV) opportunities.